Federal rescheduling handed cannabis operators a tax tool they never expected to have. Whether they use it — and how — is what the next several years of market data will settle.

In state after state, the arrival of adult-use cannabis set off a slow, measurable erosion of the medical market — not a collapse, but a steady bleed that showed up first in sales data, then in license counts, and finally in patient rolls. Michigan lost 79 percent of its medical dispensary licenses from peak. New Mexico shed a fifth of its registered patients in twelve months. The direction was unmistakable: licenses, revenues, and patients were migrating to adult use. The medical market was losing share. The cannabis market was not.

Then the federal government rescheduled cannabis — and changed the equation entirely.

Medical cannabis, now classified as Schedule III, is no longer subject to IRC Section 280E, the tax provision that has cost cannabis operators billions in disallowed deductions since the 1980s. Adult-use cannabis is not, for now, and it remains Schedule I. The same product, sold from the same building, now carries a different federal tax burden depending on which side of the dual-license ledger it lands on. That is not a nuance. That is a structural advantage — one the industry assumed medical would never have again.

Section II

The National Portrait: Four Data Streams, One Picture

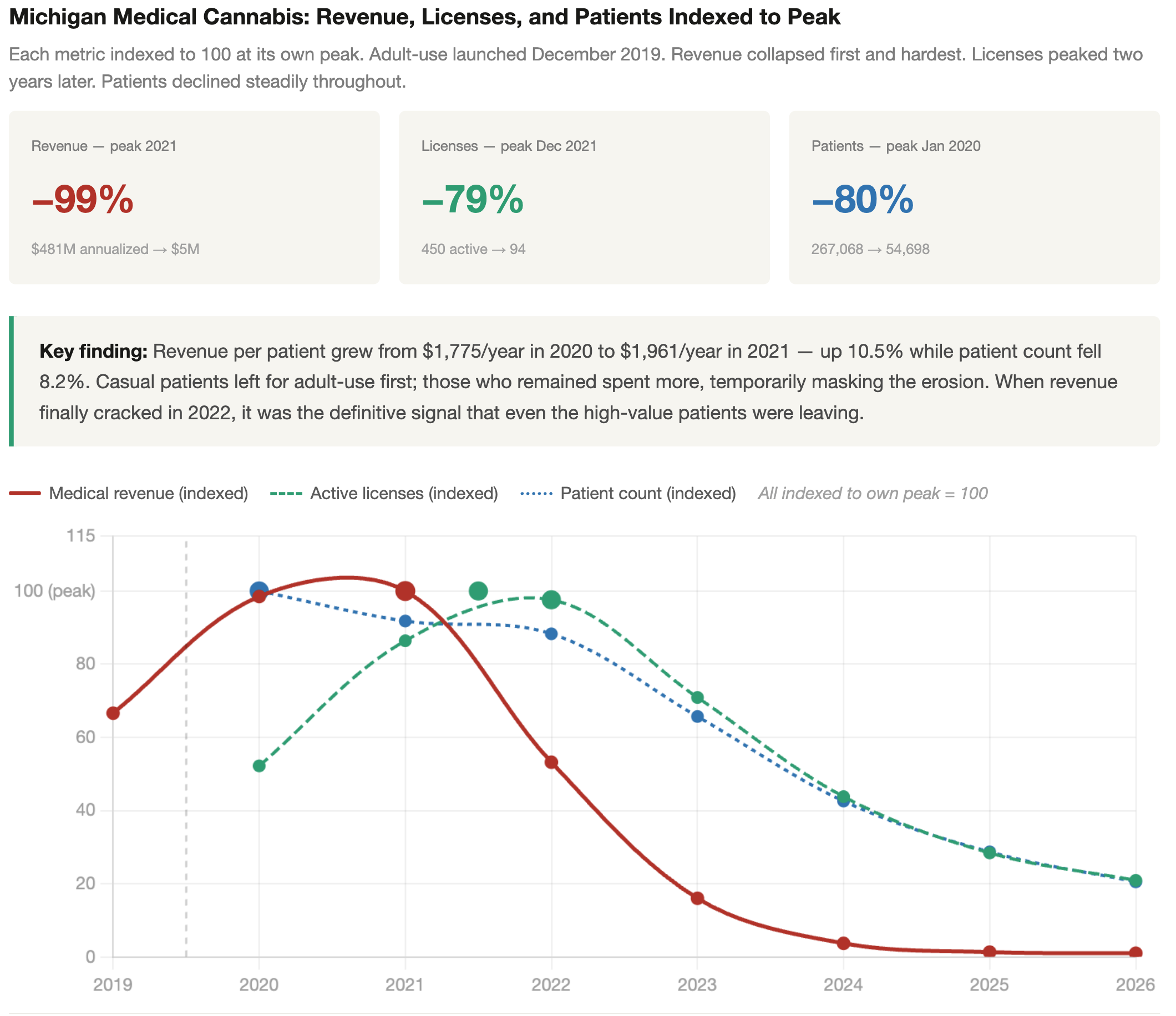

The most important analytical finding across four datasets and thirty-two reporting states is also the least intuitive one: revenue is the leading indicator of medical program health, patient counts are the lagging one, and license counts fall somewhere in between. Sales figures move first. Licenses consolidate next. Patient rolls thin last. Patient counts are the most visible metric in state regulatory reporting — updated monthly, widely cited, easy to track. But they are also the last to move. Michigan's medical program revenue peaked in 2021 at approximately $481 million annualized. Its patient count didn't reflect that peak for another two years. By the time the patient data looked alarming, the revenue signal had been flashing red for years. Understanding that sequence is the key to reading everything that follows — and to understanding what the rescheduled environment is already telling us that the patient data hasn't caught up to yet.

One additional frame before the data: in most states that launched adult-use programs, the total cannabis market grew substantially — often dramatically. Missouri's combined market nearly quadrupled in the two years following adult-use launch in 2023. Ohio more than doubled. Maryland grew by 135 percent. In many cases what followed was less a migration than a shift at the point of sale — the same customer, often the same store, a different SKU on the register. The medical market lost share. The cannabis market did not.

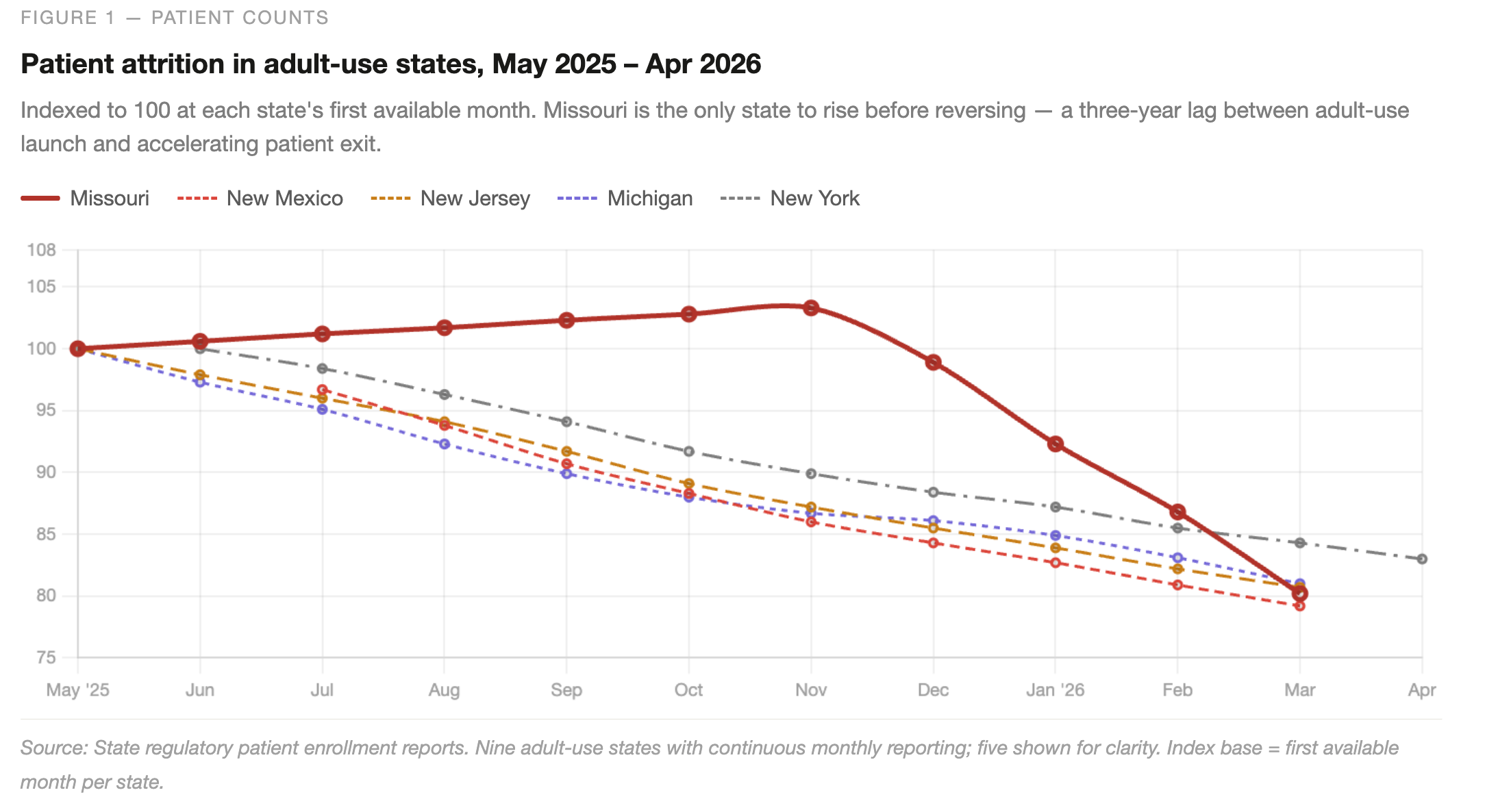

The patient enrollment data covers the most recent twelve months across thirty-two reporting states. Across the nine adult-use states with continuous monthly reporting, patient counts declined without exception — ranging from roughly 1.2 percent per month in Colorado and Arizona to more than 2.5 percent per month in New Mexico. Missouri presents the starkest single data point: enrollment rose modestly through November 2025, then reversed sharply, falling from 127,804 to 99,277 by March 2026. That reversal happened approximately three years after adult-use sales launched — consistent with the lag between revenue signal and patient signal the sequencing insight predicts. Medical-only states told the opposite story. Louisiana added nearly 200,000 patients over the same twelve months. Pennsylvania, Arkansas, and Utah all grew steadily. Where there is no adult-use channel to migrate to, the card retains its value.

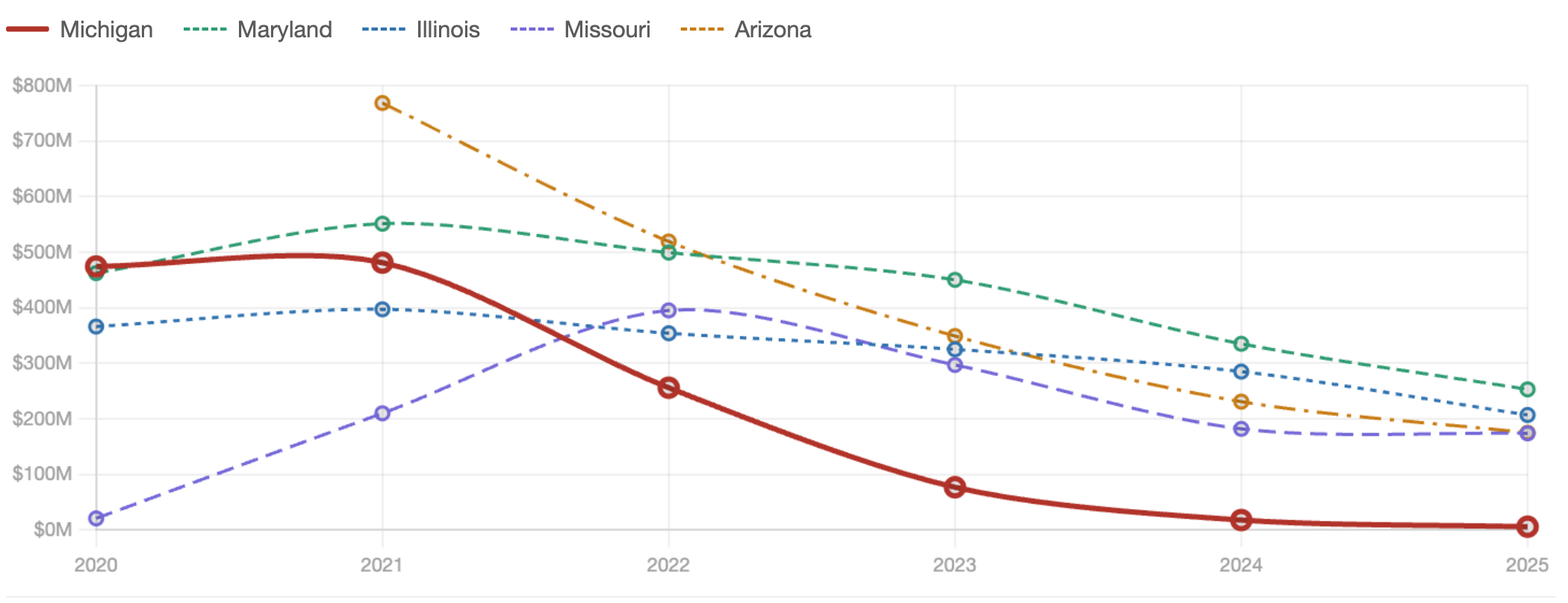

The license data, covering active dispensary counts from May 2020 through April 2026, shows the same bifurcation on the supply side. Michigan's medical license count fell from a peak of 450 to 94 — a 79 percent reduction. Colorado shed licenses steadily across the full observation window, declining from 433 to 277. Florida's medical-only program grew from 322 dispensaries to 766 over the same period. Pennsylvania expanded from 84 to 189. Oklahoma, with no adult-use program and 1,364 active licenses, represents the outer limit of what an uncapped medical-only licensing regime produces. The pattern is consistent: adult-use states consolidate, medical-only states expand.

Figure 2 — Active licenses

Medical dispensary license trajectories, 2020 – 2026

Annual May snapshot; April 2026 for current period. Adult-use states consolidate; medical-only states expand.

Source: State regulatory license data, May 2020 – April 2026. Ohio's license count went to zero in late 2024 following dual-licensure conversion — an administrative reclassification, not a market exit.

Source: State regulatory license data, May 2020 – April 2026. Ohio's license count went to zero in late 2024 following dual-licensure conversion — an administrative reclassification, not a market exit.The revenue data closes the portrait. Pennsylvania has grown medical program revenue from $306 million in 2019 to $1.8 billion in 2025 — every year, without exception, and without an adult-use competitor on the same shelf. That is the undisrupted benchmark. Every other number in this analysis is measured against it. In the most mature adult-use states, meanwhile, total combined market revenue is now compressing. Colorado's combined market is down 26 percent from peak. Arizona is down 22 percent. The growth phase is over in those markets, and margin pressure is real. The revenue signal is already showing what the patient data will confirm in twelve to eighteen months: the easy growth is behind them.

Figure 3 — Medical sales

Annualized medical program revenue, 2020 – 2025

Revenue is the leading indicator. Michigan's trajectory shows the endpoint. Pennsylvania grows every year with no adult-use competition. Missouri's 2022 peak marks the adult-use launch inflection.

Source: State medical sales reports. NJ and PA figures annualized from quarterly reports. AZ 2020 not available. Medical program revenue only.

A fourth dataset — product composition across thirteen reporting states — rounds out the consumer portrait. The medical patient's format preferences have stabilized around flower as the dominant category, with vaporizers as a secondary format. That preference profile is now consistent enough across reporting states to plan around.

Section III

The Three Clocks: Why the Data Looks the Way It Does

Understanding what the medical data is telling us requires understanding the three speeds at which cannabis markets actually move. Patients and customers vote with their dollars every transaction — the market registers their preferences immediately in revenue figures. Medical card renewals happen once a year or so; patients can continue spending at adult-use stores for months before their card comes up for renewal and they decide not to bother. And operator decisions about licenses — applying for new ones, letting old ones lapse, restructuring existing ones — run on regulatory cycles that can stretch well beyond a year. These three time horizons mean that a single market event can be simultaneously visible in the revenue data, invisible in the patient count, and entirely absent from the license count. The signals are real. They just arrive on different schedules.

The three clocks run on different schedules. Revenue signals shift at purchase speed. Patient enrollment follows at renewal speed. License counts move last, at regulatory speed.

Across adult-use states, revenue tends to register the sharpest response when market conditions shift — falling harder and faster than either patient counts or license numbers. Licenses tend to be the stickiest metric, reflecting operator confidence and positioning rather than immediate consumer behavior, and lagging revenue in every state the dataset covers. Patient counts fall somewhere between the two: more gradual than the revenue signal, more immediate than the license signal. None of this is a precise formula. Markets differ by state, by program maturity, and by how aggressively operators compete across medical and adult-use channels. But the general pattern is consistent enough to be useful as a forward-looking frame.

One finding from the data deserves particular attention because it changes how the revenue signal should be read. In the early stages of adult-use adoption, revenue can actually hold up — or even grow slightly — while patient counts are already declining. The patients who leave first tend to be the casual, lower-frequency users. The patients who stay are likely more medically motivated and higher-spending. Revenue per remaining patient rises even as the total count falls, temporarily masking the erosion. When revenue breaks, it tends to break hard, because by that point the high-value patients are leaving too. The revenue signal does not arrive first — it arrives loudest. That distinction matters for anyone trying to read market health in real time.

Revenue: annualized from monthly medical sales data. Licenses: May snapshot each year; December 2021 peak (450 licenses) falls between 2021 and 2022 labels. Patients: January of each year. Adult-use launch: December 2019. Source: state regulatory data.

The data also reveals something the three-clock framework does not fully capture: patients and consumers tend to take the path of least resistance to procurement, and they change direction faster than the annual card cycle would predict when the incentive is strong enough. The medical card is not an identity or a commitment — it is a procurement credential, held when it represents the most convenient or economical path to the product and abandoned when something easier appears. Florida offers the clearest demonstration. The state's medical program was adding tens of thousands of net new patients per year through 2023. Then, as Amendment 3 — the adult-use ballot measure — approached its November 2024 vote, enrollment collapsed. In August, the program added just 529 patients. In October, it went negative. The vote failed. By December, nearly 7,000 patients enrolled in a single month. The underlying demand for cannabis had not changed. The anticipated procurement path had — and patient behavior followed within weeks, not months.

This is the pattern that makes rescheduling analytically interesting rather than merely administratively significant. If medical operators pass the 280E savings through to pricing, patients currently renewing out of habit have a reason to stay engaged. Adults buying at adult-use stores who have never held a medical card have a reason to consider getting one. And operators who have been allowing medical infrastructure to run down have a reason to rebuild it. None of these responses happens on the same schedule. The revenue impact of lower medical pricing shows up quickly. The patient enrollment response takes until the next renewal cycle. The license and infrastructure response takes longest of all. Reading the market accurately in the rescheduled environment means knowing which clock each signal is running on.

For operators, investors, and the analysts who track this market, the practical implication is straightforward. Revenue figures are the most sensitive early signal, but they need to be read in context — a brief period of revenue stability in a declining patient market is not health, it is amplification before the drop. Patient enrollment trends, particularly net new patients rather than total count, are the most honest measure of program vitality. And license counts are the best forward indicator of where operators believe the market is going — because no one spends time and money maintaining a license they don't intend to use.

Section IV

The Undisrupted Benchmark: Pennsylvania

Pennsylvania has been growing its medical program every year since 2019 without an adult-use competitor on the same shelf. That fact carries more analytical weight than it might appear to. Every other major medical program in the country is either operating alongside an adult-use market it helped create, or waiting for one to arrive. Pennsylvania is neither. It is the closest approximation the data offers to a controlled environment — a well-capitalized, well-enrolled program running exactly as its architects intended, with no external variable distorting the count.

The results are on record. Program revenue has grown from $306 million in 2019 to $1.8 billion in 2025, a compound run that no dual-market state has matched on the medical side of its ledger. Patient enrollment stands at 439,000. Active dispensary licenses number 189, up from 84 at program maturity — a doubling that tracked demand rather than raced ahead of it. All three clocks are running in their expected sequence. Revenue led. License issuance followed. Enrollment trailed in the normal order. There is no divergence to explain.

That sequencing is worth pausing on precisely because it is absent elsewhere in the data. In Michigan, the purchase clock collapsed before the card clock registered the change — revenue fell while enrollment held, then enrollment fell while licenses held, producing the cascade of divergence that the three-clocks framework is designed to read. The clocks spread apart because adult-use disrupted each variable at a different lag and at a different speed. In Pennsylvania, no such disruption occurred. Revenue growth pulled licensing investment behind it. Licensing investment pulled patient outreach behind that. The program compounded on itself in the way medical programs are theoretically supposed to, and the credential retained its value because no cheaper path ever opened beside it.

Pennsylvania borders New York, New Jersey, Delaware, Maryland, and Ohio — all adult-use states. West Virginia, the lone medical-only exception, shares only a short border. That Pennsylvania's medical program has grown every year in that geography makes it the most meaningful benchmark in the dataset.

The $1.8 billion figure is therefore not simply a revenue number. It is a ceiling estimate for what an undisrupted medical program can produce in a large, demographically diverse state across a six-year run. It is also a reference point: for operators considering a deliberate pivot toward the medical market in dual-market states, Pennsylvania is what the upside looks like when the card economics hold and the competitive environment stays closed. Whether a mature adult-use state can retrace any portion of that path — through 280E relief, disciplined pricing, or some combination of the two — is the question the following sections take up directly.

Section V

Rescheduling, §280E Relief, and the Card Economics

The Internal Revenue Code's §280E provision has functioned as a punitive excise on cannabis operators, compressing effective after-tax margins to levels unviable in any comparably regulated consumer-goods category. The rescheduling question is therefore not merely symbolic. Movement to Schedule III would sever the §280E linkage, restoring the full apparatus of normal business deductibility — a structural shift in the operator's income statement rather than a marginal improvement to it.

The transmission from deductibility to retail price runs through competitive margin dynamics. In the near term, rescheduling creates a margin windfall for existing operators. In a concentrated market with high barriers to entry, incumbents retain the surplus; in a competitive market with low buyer switching costs, the surplus is competed away into price. Cannabis retail occupies intermediate ground — competition is real but bounded by licensing constraints — so the expectation is partial and uneven pass-through, with the degree determined by local competitive density and proximity to license saturation.

Where pass-through does occur, it directly perturbs the card economics Section IV left unresolved. The medical cardholder's willingness to maintain the credential rests on a price differential sufficient to offset the card's transaction costs — renewal fees, physician certification, the friction of a parallel purchasing channel. If §280E relief compresses adult-use retail prices toward medical-program price points, that differential narrows. Narrowing reduces the card's economic return without eliminating it; full elimination requires the differential to close entirely, which is unlikely given that medical programs typically carry their own excise structures and, in some states, product-type price floors.

Pennsylvania's trajectory becomes legible through this frame. The state's adult-use transition will inherit whatever margin structure rescheduling has established by the time it launches. If §280E relief precedes adult-use authorization — a plausible sequencing given federal legislative timelines — operators entering that market will do so with a fundamentally different cost basis than their counterparts in earlier-converting states faced. How long the dual-market period lasts, and whether the medical credential holds its value through it, will depend in part by a federal tax decision that most state-level market analyses don't bother to model.

Section VI

Dual-Market States as Leading Indicators

The three forces examined above don't arrive in sequence — they operate at the same time, and their overlap is what makes dual-market states worth watching beyond their own borders.

Consider what medical patients actually do after adult use arrives. A meaningful share keep their cards. Product access doesn't explain it — adult-use shelves often carry the same goods. What it does suggest is that some patients still find formal status worth holding when federal exposure remains a real concern, and that concern doesn't disappear under Schedule III reclassification, it only shrinks. States with several years of post-transition enrollment data are in a position to show what that shift looks like before it becomes visible elsewhere.

Pennsylvania adds a different dimension. When the state eventually moves to adult use, it won't simply be adding a new consumer class — it will be carrying forward pricing norms, operator relationships, and regulatory habits built around a captive medical market. The subsequent price path and operator shakeout will trace territory that earlier-converting states never traveled, because none of them started from a medical base this large and this established.

The 280E question runs through both. Tax relief improves margins in the short run, but it doesn't resolve the competitive pressure that adult-use entry creates — it shifts where that pressure lands and when.

Taken together, these states are better read as early evidence than as finished cases. What looks like a stable present condition in a dual-market state is more accurately described as a point in a process — incomplete federal resolution, patients still weighing their options, operators still positioning — that every state moving toward adult use will eventually have to work through.

Section VII

Oklahoma: When the License Clock Runs Backward

Oklahoma built the most crowded medical cannabis market in the country. At its peak the state had issued 2,877 dispensary licenses — the highest per-capita count of any regulated cannabis market, medical or adult-use, in the United States. The economics that followed were predictable: too many operators chasing a finite patient base produced margin pressure, consolidation, and a significant share of licenses held by operators running at or below breakeven. The state's response was a moratorium on new licenses, which has been in place long enough that the count is now falling by attrition.

What makes Oklahoma analytically useful is that the moratorium separated the license clock from the other two. Revenue and enrollment are still running — $646 million in annual medical sales, 311,000 registered patients — while the license count shrinks. That is the reverse of what the data shows in adult-use transition states, where revenue and patients fall first and licenses lag behind. In Oklahoma, a regulatory decision moved the license clock independently of the market. The question the next few years will settle is whether revenue and enrollment hold at a smaller, more rational operator count, or whether they follow the licenses down as the market thins.

Section VIII

Florida: The Largest Test Case Has Not Run Yet

Florida is the largest medical cannabis market in the country by patient count — 918,000 registered patients, 766 dispensary licenses, and a vertically integrated operator structure that has produced some of the densest retail footprints in American cannabis. Trulieve alone operates more than 130 stores. The license count looks small relative to Oklahoma or Colorado, but the unlimited-stores-per-license model means the physical retail infrastructure is already built at scale. When adult-use launches, Florida's operators will not need to expand — they will need to redirect.

That distinction matters for how the transition will read in the data. In every prior adult-use conversion in the dataset, the license clock lagged because operators had to apply, wait, and build. Florida compresses that lag to near zero. The purchase clock and the card clock will start moving the day adult-use goes live, but the infrastructure is already there. The result may be a sharper and faster divergence between revenue and patient enrollment than any prior state has produced — not because the market is weaker, but because it is too mature to absorb the transition gradually.

Section III's Florida enrollment data already showed how quickly patient behavior responds to an anticipated change in the procurement path. Enrollment collapsed in the months before the November 2024 adult-use vote and rebounded sharply when the measure failed. That pattern will run in the other direction when adult-use eventually clears, and the first twelve months of post-launch data will be the most closely watched cannabis market signal in years.

What the existing data cannot answer is how the rescheduled environment interacts with Florida's specific operator structure. Vertically integrated operators with large medical footprints have more to gain from 280E relief — and more to lose from adult-use price compression — than any other operator category in the country. Whether they use the tax advantage to defend medical pricing, or allow it to be competed away through the adult-use channel, will play out store by store and quarter by quarter.

The broader pattern the data suggests is less complicated than the individual state stories make it appear. Medical cannabis eroded not because it failed, but because something faster and easier appeared beside it. The markets that held — Pennsylvania, Oklahoma under the moratorium, Florida before adult-use arrived — held because that easier path either hadn't been built or hadn't been made legal. Rescheduling changes the economics without changing that underlying logic. It gives operators a concrete reason to invest in the medical channel at a moment when most had stopped. Whether they recognize it and act on it is what the next several years of data will answer.

Emerald Intel · Draft — Not for distribution · May 2026